All Purdue Distributions Were Proper

Court filings have incorrectly claimed that Purdue and the Sackler family were aware of potentially insurmountable lawsuits and liabilities when approving distributions of the company’s profits. Those allegations are demonstrably false.

Media coverage has also ignored the indisputable fact that about half of the distributions made by Purdue were for the purpose of paying government taxes and questioned the accuracy of the amount of distributions (despite detailed financial records being filed with the bankruptcy court and shared with Congress.

All Distributions Were Legitimate — Purdue Always Had Ample Cash

Distributions to the Sackler family were entirely appropriate:

- Purdue never had any meaningful debt.

- Every year there were distributions, hundreds of millions of dollars in cash remained in the company.

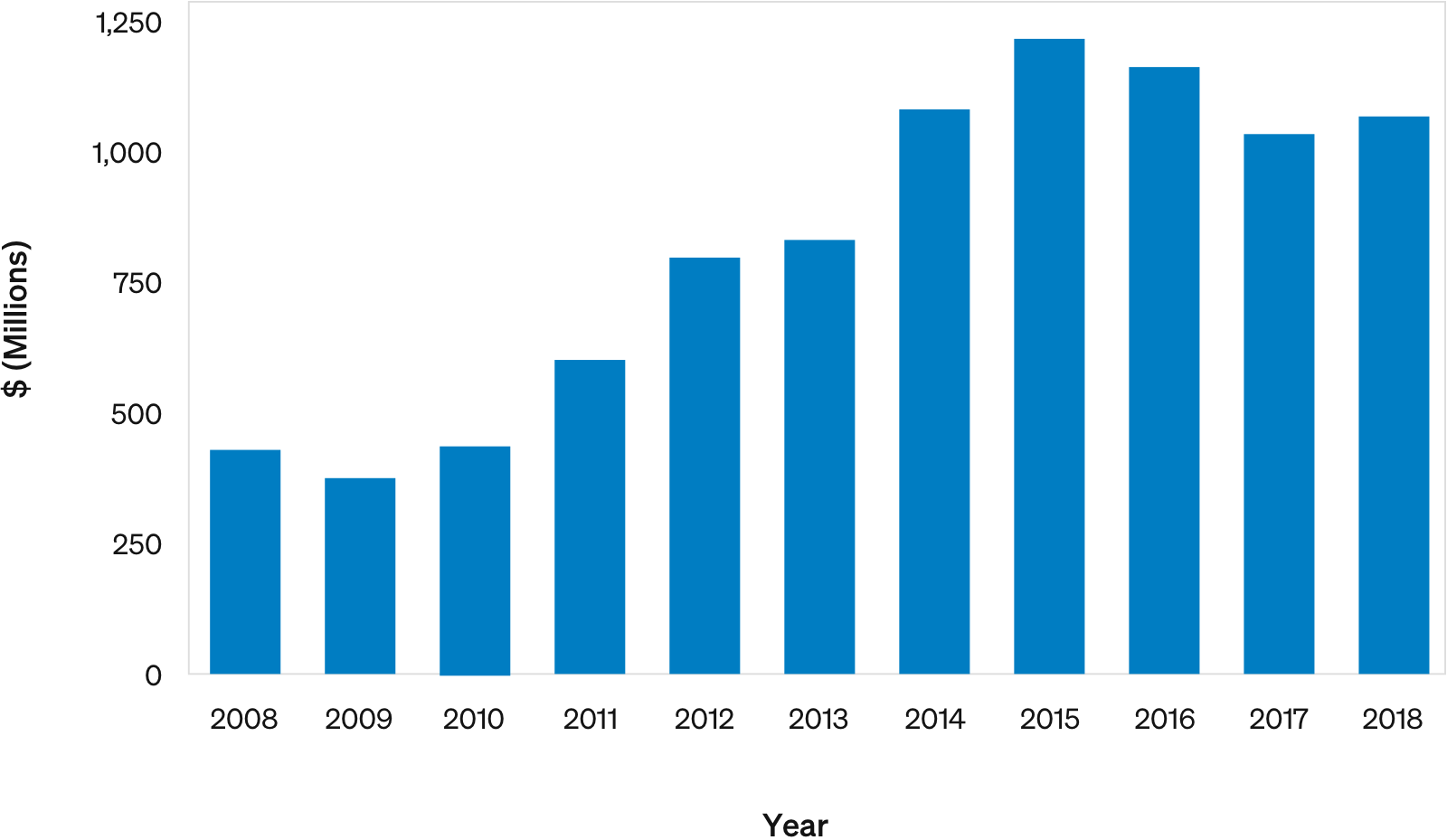

- From 2014 on, there was over a billion dollars a year of cash in Purdue every year—after distributions.

- None of the opioid-related lawsuits that led to Purdue’s bankruptcy were filed until 2014, and there was only a handful until 2017.

- Only in 2017 did a huge wave of litigation strike, and distributions then ended.

Substantial Amounts of Unrestricted Cash on Hand Remained at Purdue After Distributions

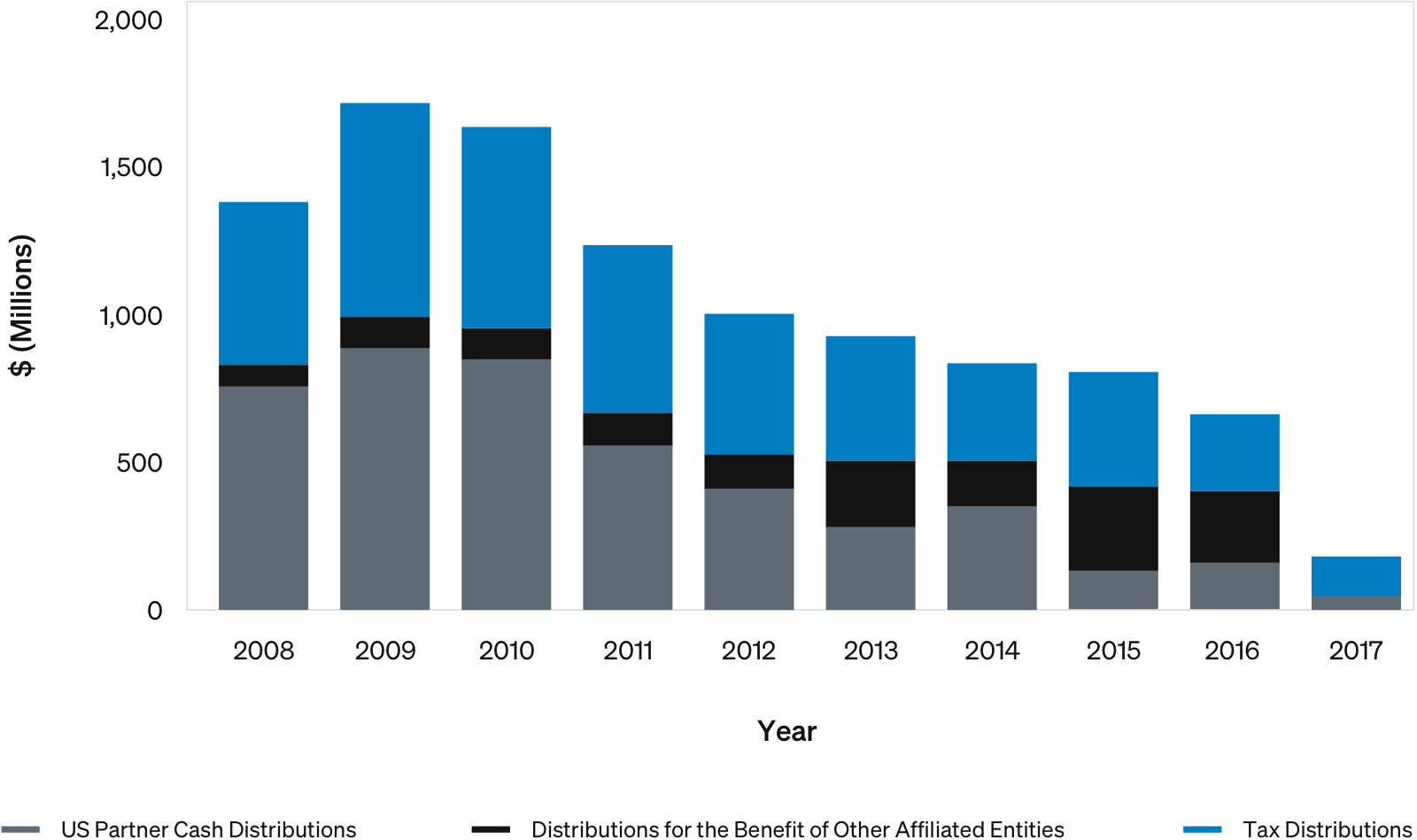

More Than Half of Sackler Family Distributions Went to Taxes & Reinvestment in Companies to Be Sold in Pending Settlement

Between 2008 and 2017, approximately $10.4 billion of cash was distributed by Purdue to, or as directed by, the Sacklers. See Debtor App. 337a Nearly half of that money was distributed to pay taxes on Purdue’s earnings (Purdue was a “passthrough” entity taxed at the owner rather than the entity level) and so primarily went to the federal government and other taxing authorities. See id. Contra Stay Appl. 8. The enhanced settlement requires the Sacklers to repay at least 97% of the non-tax cash distributions made to them in the nearly 12 years prior to the bankruptcy filing.

DEBTOR’S RESPONSE IN OPPOSITION TO APPLICATION FOR A STAY OF THE MANDATe OF THE UNITED STATES COURT OF APPEALS FOR THE SECOND CIRCUIT PENDING THE FILING AND DISPOSITION OF A PETITION FOR A WRIT OF CERTIORARI (PG. 10-11), AUGUST 4, 2023 [1]

The $10.3 billion in distributions (45% of which was paid to the government in taxes) that became public in October 2019 had been fully disclosed to all the states, local governments and other plaintiffs in 2018. Every party that agreed to the settlement knew all about the distributions. (The Sackler family is contributing its ownership of Purdue – whose future profits are dedicated to addressing opioid addiction – plus at least an additional $6.5 billion to help communities and people in need.[2])

Distributions Declined Starting in 2009 & Ceased Once Wave of Litigation Emerged 2017

Purdue/Rhodes Total Cash Distributions to or for the Benefit of IACs and Taxing Authorities[3]

Distributions Occurred Before Wave of Litigation Emerged in 2017

The company had previously settled all claims with the federal government and every state by 2007. Before 2017, Purdue’s management assured the Board that the risk of litigation was low.

Purdue did not face meaningful litigation until 2017.

From 2008 to 2012, Purdue was under a federal monitorship—and any litigation at that time was both manageable and resolved.

Of the few opioid lawsuits against Purdue prior to 2017, none threatened Purdue’s solvency.

- Purdue settled an investigation by New York State for $75,000.

- Purdue settled a lawsuit by Kentucky for $24 million over eight years.

Until this current round of litigation, Purdue had resolved all cases and inquiries for reasonable sums.

Purdue ceased making distributions once the “wave” of litigation began in 2017.

Purdue’s distributions were never more than a fraction of Purdue’s sales revenues.

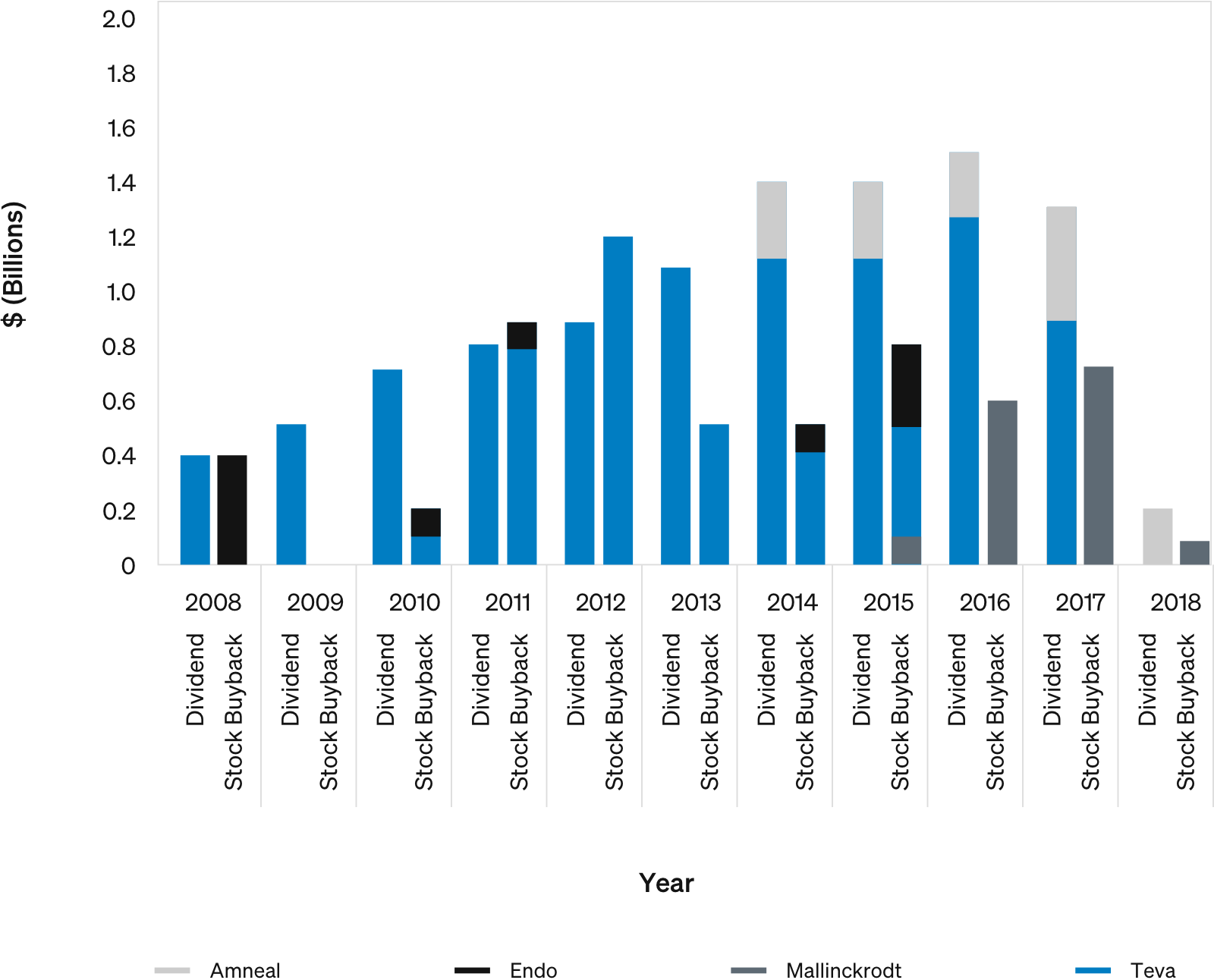

Publicly Traded Opioid Manufacturers Did Not Believe Opioid Marketing Liability Was Foreseeable Risk Before 2018

Mallinckrodt, Endo, Teva, nor Amneal included opioid-marketing litigation as a risk factor in their 10-Ks until 2018.

Historical Dividend Payments and Stock Buybacks

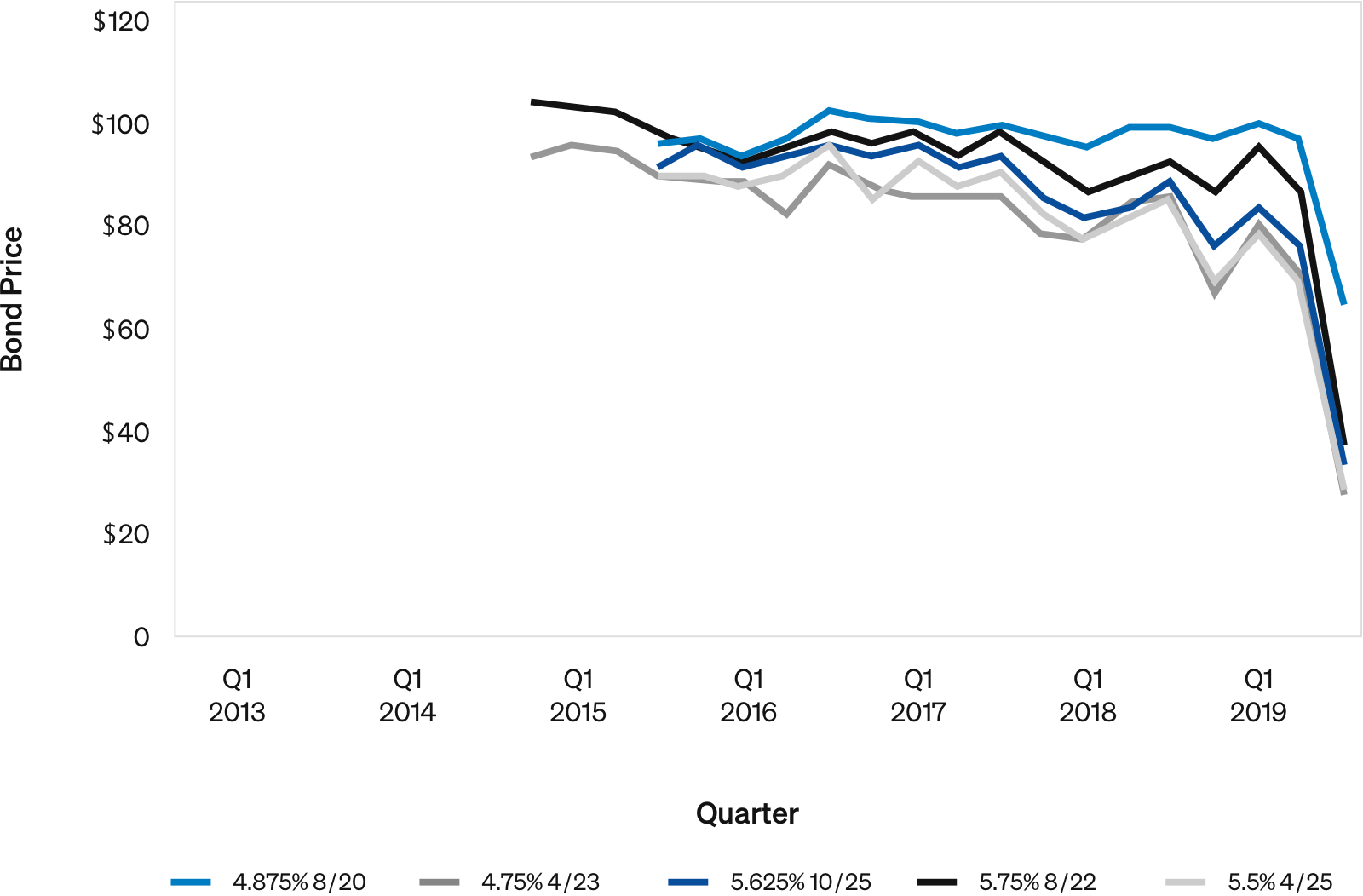

Bond Prices for Comparable Companies Confirm Debt Markets Did Not Perceive Substantial Credit Risk From Opioid Litigation Until 2018 or 2019

Example: Mallinckrodt International Finance S.A.

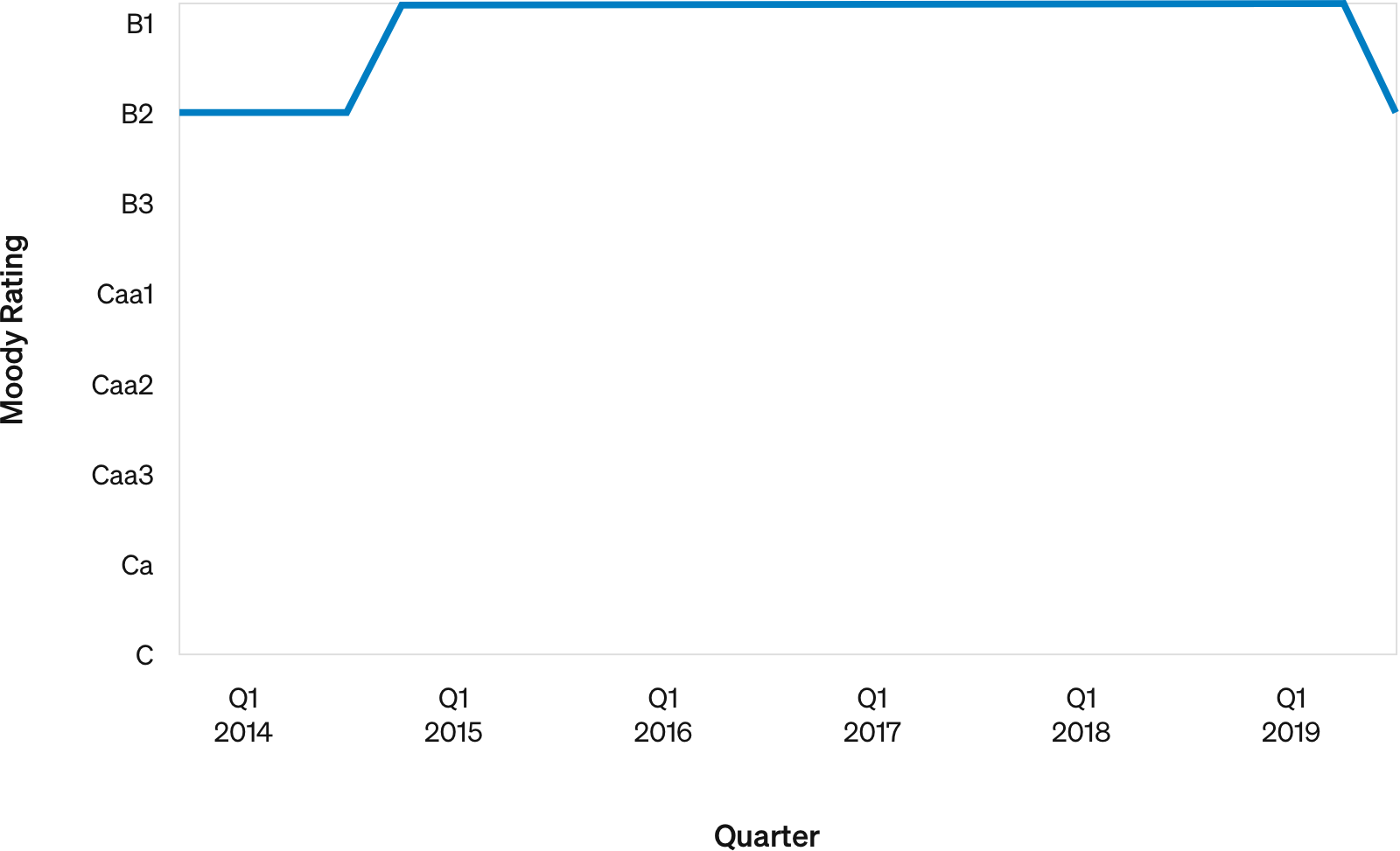

Credit Rating Agencies Did Not View Opioid Litigation As Basis for Public Company Downgrades Until 2019

Example: Quarterly Ratings by Moody’s for Amneal Pharmaceuticals

SEC Disclosures Did Not Include Risk of Opioid Litigation As Risk of Financial Health Until 2017

Number of Opioid-Matter Disclosures

| Year Disclosed | MNK | ENDP | TEVA | AMRX |

|---|---|---|---|---|

| 2013 | 0 | No 10K | No 10K | No 10K |

| 2014 | 0 | No 10K | No 10K | No 10K |

| 2015 | 0 | 0 | No 10K | No 10K |

| 2016 | 0 | 0 | No 10K | No 10K |

| 2017 | 0 | 0 | No 10K | No 10K |

| 2018 | 1 | 1 | 0 | No 10K |

| 2019 | 2 | 4 | 1 | 1 |

Emails About “Distributions” Were Actually About Keeping Money in Purdue

A series of emails among Sackler family members are inaccurately described as advocating for additional cash distributions from the company. In this example, Jonathan Sackler was, in fact, urging that additional funds remain inside the company.

Paragraphs 160-162

False Claim

“… Jonathan Sackler emailed David Sackler, Richard Sackler, and a long-time financial advisor, stating that an investment banker once told him, ‘your family is already rich, the one thing you don’t want to do is to become poor.’”

The same day, David Sackler replied-all by email: “[W]hat do you think is going on in all of these courtrooms right now? We’re rich? For how long? Until which suits get through to the family? I think [the investment banker’s] advice was just violated in a Virginia courtroom. My thought is to lever up where we can, and try to generate some additional income. We may well need it… Even if we have to keep it in cash, it’s better to have the leverage now while we can get it than thinking it will be there for us when we get sued.”

In or about April 2008, Richard Sackler wrote a memorandum to Kathe Sackler, Ilene Sackler, David Sackler, Jonathan Sackler, and Mortimer D. A. Sackler in which he discussed limiting the Sackler family’s risk in the ownership of Purdue: “[T]he most certain way for the owners to diversify their risk is to distribute more free cash flow so they can purchase diversifying assets.”

Fact

This email exchange is focused on how to manage money and whether to use leverage, not how much to take from Purdue.

- David Sackler, before he was on Purdue’s board, notes that “as someone of a different generation (a) little leverage here and there is a good thing.”

- Jon Sackler provides an analysis of the “wonderful run for asset values” asking, “Will that continue forever?” and how to hedge against market swings.

- As for a brief speculative reference to potential lawsuits naming family members, Jon sums that up this way: “you should rest assured that there is no basis to sue ‘the family.’”

- In an April 2008 memorandum to the Board, the risk Richard Sackler was discussing referenced the exclusivity for OxyContin expiring in 2013 as of that time.

Paragraph 164

False Claim

The same day, Jonathan Sackler responded to Mortimer D. A. Sackler that “when the business has more cash flow than is required, I’ve supported distributions, and we’ve taken a fantastic amount of money out of the business.”

Fact

- Jon Sackler provides a full-throated argument against distributing in favor of keeping cash inside the company.

- Jon then acknowledged being a “little heated” during an earlier meeting when he argued against distributions, concluding: “I feel a sense of obligation to keep the companies strong, not just for us and our children, but also for the people who’ve thrown in their lot with us.”

- It is disappointing the government has completely mischaracterized this email exchange by using out-of-context quotes.

Paragraph 165

False Claim

About a month later, on October 12, 2014, Jonathan Sackler emailed Richard Sackler, David Sackler, and others: “I think we can continue to make money in it [opioid analgesics] for decades to come, particularly if we are smart and diligent around emerging markets, formulation, generics, and APIs, but in the aggregate, it’s more of a smart milking program than a growth program.”

Fact

- This is another example of the government suggesting an email exchange means the opposite of what the words actually say.

- Jon actually opens the email saying his views are “probably simplistic” because he’s “unfamiliar with strategy as a discipline.” He then talks about how Purdue “stumbled into opioid analgesics” and that future growth would likely be limited because Purdue is not likely to invent substantial new products.

- The reference to “smart milking program” is an acknowledgment that profits are likely to decline due to “brand and price competition and price sensitivity.“

- Put simply, this email exchange has absolutely nothing to do with selling more OxyContin.